The 2026 Blueprint: How Middle and Upper-Class Americans Really Invest for Retirement

take precautions

Salamon and Salamon

3/19/20263 min read

Executive Summary

The American retirement model in 2026 is built on a framework of individual agency and strategic financial planning. Moving beyond reliance on state-provided safety nets, the system utilizes a "three-legged stool" approach—Social Security, employer-sponsored plans like 401(k)s, and private savings—to ensure long-term stability. This report highlights the importance of tax-advantaged vehicles, such as Roth IRAs and HSAs, and the necessity of diversifying into equities and real estate to outpace inflation. By applying the "25x Rule" and disciplined capital allocation, individuals can bridge the gap between basic government benefits and the capital required to sustain a middle-to-upper-class lifestyle. Ultimately, retirement success in the U.S. is not a product of luck, but the result of systematic tax optimization and long-term participation in the growth of the American economy.

Introduction

The "American Dream" of a peaceful retirement—one with a paid-off home, a reliable car, and the freedom to enjoy weekends—is not a matter of luck in 2026. It is a matter of calculated financial engineering. Contrary to popular belief, Americans do not rely solely on the government. Instead, they use a sophisticated mix of tax-advantaged accounts, real estate, and diversified portfolios to build their nest eggs.

Whether you are looking to understand the system or emulate it, here is the breakdown of how the U.S. middle and upper classes plan their exit from the workforce.The Retirement "Three-Legged Stool"

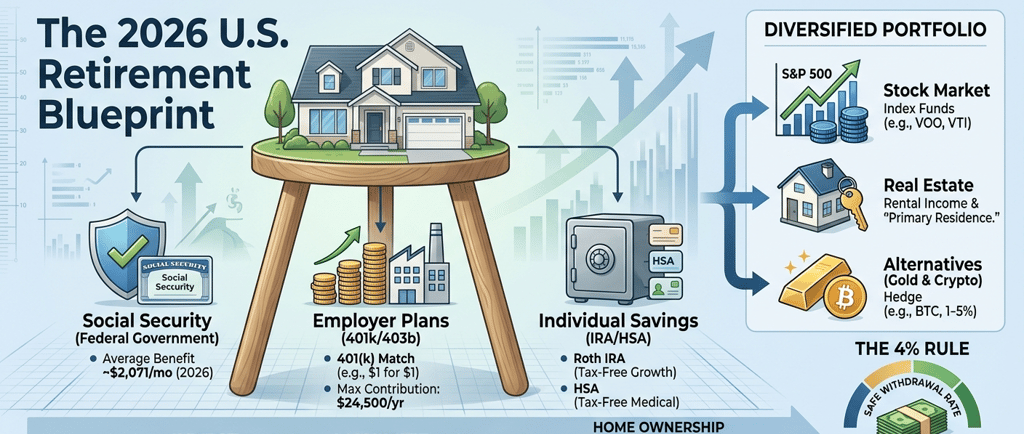

The modern American retirement strategy rests on three primary pillars: Social Security, Employer-Sponsored Plans, and Individual Savings.

Pillar I: Social Security (The Baseline)

Social Security is the government’s safety net. In 2026, the Full Retirement Age (FRA) is now 67 for anyone born in 1960 or later.

The Reality Check: The average monthly benefit in 2026 is approximately $2,071. For a middle-class lifestyle, this is rarely enough to cover more than basic utilities and groceries.

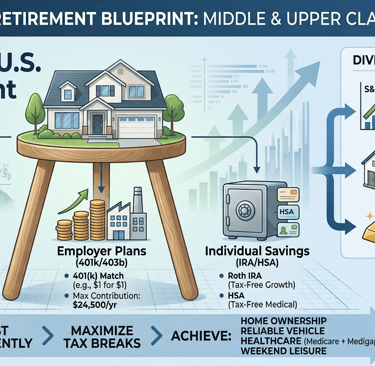

Pillar II: The 401(k) and 403(b) (The Wealth Engine)

This is where the middle class builds its core wealth. Employees contribute a portion of their salary before taxes.

2026 Contribution Limit: $24,500 per year (plus an $8,000 "catch-up" for those over 50).

The Benefit: Many employers offer a "match" (e.g., they put in $1 for every $1 you contribute up to 6%). It is essentially an immediate 100% return on investment.

Pillar III: IRAs and HSAs (The Tactical Tools)

IRA (Individual Retirement Account): In 2026, individuals can put up to $7,500 into these accounts. The Roth IRA is a favorite among the upper-middle class because you pay taxes now, but the money grows and is withdrawn 100% tax-free in retirement.

HSA (Health Savings Account): With the rising cost of American healthcare, the HSA is vital. Contributions are tax-deductible, and withdrawals for medical expenses are tax-free.

High-Growth Investments: Stocks, Real Estate, and Crypto

To maintain an upper-class lifestyle, Americans diversify into assets that outpace inflation.

The Stock Market (Equities): Most portfolios are anchored in Low-Cost Index Funds (like those tracking the S&P 500). Historically, these provide a 7-10% annual return.

Real Estate: For the middle class, the "Primary Residence" is the biggest asset. The upper class often owns Rental Properties. Under U.S. law, the "1031 Exchange" allows investors to sell a property and reinvest the profit into a new one without paying immediate taxes.

Alternative Assets: In 2026, it is common for diversified portfolios to hold 1% to 5% in Cryptocurrencies (like Bitcoin) or Gold as a hedge against currency devaluation.

Taxes: What the "Taxman" Takes

Understanding the IRS (Internal Revenue Service) rules is the difference between a "comfortable" and a "struggling" retirement.

Investment TypeFederal Tax Treatment

Traditional 401(k)/IRA Taxed as Ordinary Income (10% to 37%) upon withdrawal.

Roth 401(k)/IRA Tax-Free withdrawals if held for 5+ years and age 59½+

Long-Term Capital Gains Assets held >1 year (Stocks, Crypto, Real Estate) are taxed at 0%, 15%, or 20% depending on income.

Short-Term Capital Gains Assets held <1 year are taxed at your standard Income Tax rate

The "Magic Number": How Much is Enough?

To have a "peaceful" life in 2026—owning a home, a car, having quality health insurance (Medicare + Medigap), and enjoying leisure—financial advisors often point to the 25x Rule.

If you want to spend $60,000 a year in retirement (above what Social Security pays):

Goal: You need a nest egg of $1,500,000.

The 4% Rule: This allows you to withdraw $60,000 annually, adjusted for inflation, with a high probability that your money will last 30 years.

Conclusion: Planning for a "Quiet Life"

A comfortable American retirement isn't about luxury yachts; it’s about stability. By starting early (ideally in your 20s or 30s), maximizing employer matches, and leveraging the tax-free growth of Roth accounts, the "basic" dream of a house, a car, and a stress-free weekend is achievable. In the U.S. system, the government provides the floor, but you must build the ceiling.

Selected Bibliography

Internal Revenue Service (IRS). Publication 590-A: Contributions to Individual Retirement Arrangements (IRAs). (2026).

Social Security Administration. Fact Sheet: 2026 Social Security Changes. (January 2026).

Vanguard Group. How America Saves: A Report on Long-Term Retirement Planning. (2026).

Investment Company Institute (ICI). The Role of Defined Contribution Plans in U.S. Retirement Security. (2026).

Munnell, A. H., & Chen, A. The 4% Rule and Sustainable Withdrawal Rates in the 2026 Economic Environment. (Journal of Financial Planning, 2026).

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy