The American Dream, Stone by Stone: Investing in US Real Estate

Investing in the US Real Estate Market: Opportunities and Challenges

Salamon and Salamon

3/14/20263 min read

Executive Summary

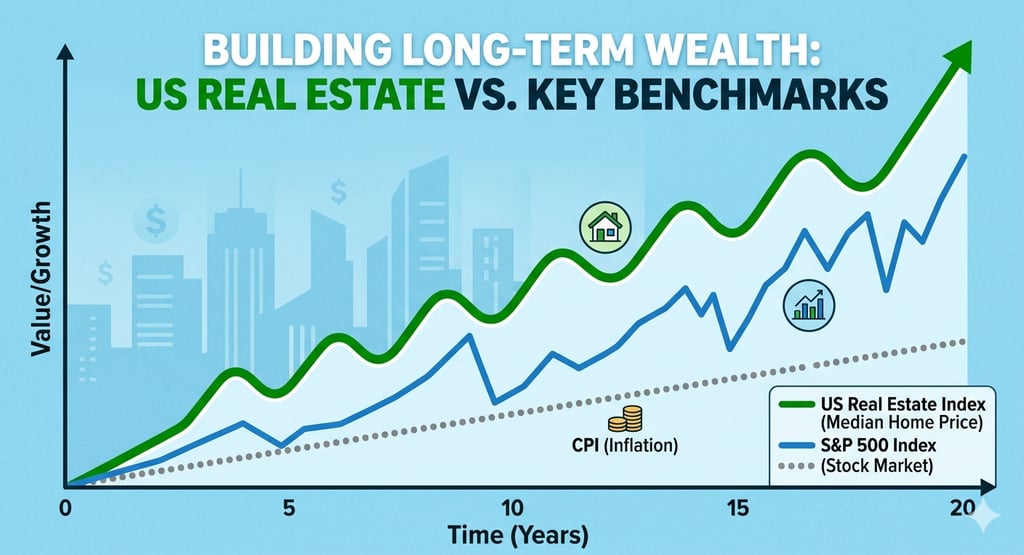

The American real estate market has evolved from a symbol of domestic stability into a premier global asset class for international and sophisticated investors. As of June 2026, the sector offers a unique trifecta of legal protection, US Dollar-denominated security, and high liquidity. This report outlines why foreign direct investment in US property—ranging from Single-Family Rentals (SFR) in high-growth "Sun Belt" regions to institutional-grade Real Estate Investment Trusts (REITs)—serves as a fundamental hedge against local market volatility. By leveraging the transparency of the US legal system and the resilience of the world’s largest economy, investors can build portfolios "stone by stone," effectively transitioning from passive observers of the American Dream to active participants in the wealth-generation mechanisms that define it.

Introduction

For decades, the "American Dream" was defined by the white picket fence—a symbol of personal success and residential stability. Today, that narrative has shifted. For the global investor, the American Dream is no longer just about a place to live; it is about a premier asset class that offers a unique combination of legal security, currency hedges, and long-term capital appreciation.

In an era of digital volatility, US real estate remains the "stone by stone" foundation of a sophisticated portfolio.

The Structural Advantages of the US Market

The United States remains the top destination for foreign direct investment in real estate for several structural reasons that go beyond simple supply and demand.

Unrivaled Property Rights: The US legal system provides some of the strongest protections for property owners in the world. Title insurance, clear zoning laws, and a transparent judicial process ensure that your "stone" is legally shielded.

A Hedge in US Dollars: Holding real estate in the US means your asset is denominated in the world’s reserve currency. For international investors, this provides a critical layer of protection against local currency devaluation.

Market Liquidity: Unlike many international markets where selling a property can take years, the US residential and commercial markets are highly liquid, supported by a massive network of institutional buyers and sophisticated financing options.

Diversification Strategies: Finding Your Niche

Building a real estate portfolio requires more than just capital; it requires a specific thesis. Depending on your risk appetite, several paths exist:

Single-Family Rentals (SFR): This is the classic "buy and hold" strategy. By targeting high-growth "Sun Belt" states or areas with strong tech and medical job hubs, investors can secure steady cash flow and significant appreciation.

Multifamily Synergy: Investing in apartment complexes allows for "economies of scale." Managing 20 units under one roof is often more efficient than managing 20 scattered houses, and it offers a buffer against individual vacancies.

Real Estate Investment Trusts (REITs): For those who prefer a "hands-off" approach, REITs allow you to invest in massive portfolios of commercial or industrial real estate without the need to manage a single tenant.

The Role of Macro-Economic Timing

While real estate is often viewed as a long-term play, timing the entry is crucial. Current market conditions—driven by a shortage of housing inventory and fluctuating interest rates—have created a "buyer’s market" for those with high liquidity. As the Federal Reserve navigates the "soft landing" of the economy, investors who move now are positioning themselves to capture the next upswing in valuations.

Conclusion

The transition from the traditional pension mindset to the private-enterprise approach has reshaped the American retirement experience. While the individual bears the burden of market volatility and sequence-of-returns risk, the historical upside of this model—when paired with proper tax strategy and consistent diversification—has proven to be more robust than many stagnant state-led systems. The "Personal Responsibility Dividend" is the ultimate outcome for those who leverage the legal framework of 401(k)s, Roth accounts, and HSAs to their advantage. Ultimately, retirement in the U.S. remains a personal project; it is the culmination of decades of disciplined capital allocation. As demographics continue to shift and the global economic landscape evolves, the investors who prioritize tax-free growth and liquidity will be the best positioned to thrive, moving beyond the safety net and into a state of true financial independence.

Selected Bibliography

Internal Revenue Service (IRS). Retirement Plans and Tax Considerations for the 2026 Fiscal Year. (2026).

Vanguard Group. How America Saves: 2026 Report on Defined Contribution Plans. (2026).

Social Security Administration. The Future of Social Security: Solvency and Demographic Challenges. (2026).

Investment Company Institute (ICI). The Role of IRAs and 401(k)s in the American Retirement System. (2026).

Munnell, A. H. The End of the Traditional Pension: A 40-Year Retrospective. (Journal of Retirement, 2026).

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute financial, legal, or investment advice. All real estate investments carry inherent risks, including the potential loss of principal. Market conditions can change rapidly, and past performance is not a guarantee of future results. Any investment decision remains the sole responsibility of the investor. We strongly recommend consulting with qualified financial and legal professionals before making any investment.

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy