The Business of War Who Loses and Who wins

Who is Profiting and Who is Paying the Bill and the Middle East?

ECONOMYWORLD

By Marcelo Salamon

5/24/20269 min read

Executive Summary

The conflicts in Ukraine and the Middle East have established a new paradigm of "asymmetric war financing," functioning as massive macroeconomic vacuum pumps that redistribute wealth from public taxpayers to specialized defense and energy sectors. While material destruction is concentrated on the front lines, financial surpluses are captured by corporate entities thousands of miles away. The United States has reinforced its industrial and energy hegemony, with LNG exporters and defense contractors (Lockheed Martin, RTX, etc.) recording record revenues as congressional aid packages effectively double as domestic industrial policy. Conversely, Europe has borne the structural cost of this realignment through deindustrialization and energy-intensive imports, while Russia faces a precarious "war-economy" hypertrophy. Ultimately, the global balance sheet demonstrates that the economic outcomes of modern conflict are mathematically asymmetric: the front-line states face generational reconstruction liabilities, while the "owners of the production infrastructure" consolidate permanent capital gains.

Introduction · The Asymmetric Financing Model: From Ukraine to Israel

Modern large-scale conflicts have established a new paradigm of financial and diplomatic engineering, serving as highly efficient mechanisms for the global redistribution of wealth. The traditional doctrine—where a single nation shoulders the financial burden of its own battlefields—has been replaced by a system of asymmetric war financing. Under this model, material costs are globalized, while industrial profits remain highly concentrated.

The military escalation in Israel post-2023 and the war of attrition in Ukraine that began in 2022 share this exact macroeconomic blueprint. In the Middle East, Israel’s military mobilization has strained its public finances, with the cost of the conflict exceeding tens of billions of dollars in operational expenses, reservist call-ups, and high-tech air defense. However, much like in Eastern Europe, a crucial slice of this effort is sustained by multi-billion-dollar foreign aid packages approved by the U.S. Congress. This shields the domestic economy from an immediate fiscal collapse while injecting capital directly back into Western defense contractors.

These two theaters of operation act as massive accelerators of global demand. According to the Organization for Economic Co-operation and Development (OECD), the negative impact of the Ukrainian conflict alone on global economic output had surpassed a monumental $2.8 trillion by the end of 2023. When combined with the economic fallout in the Middle East—which disrupted vital shipping lanes in the Red Sea, inflated international maritime freight rates, and kept commodity risk premiums high—the global financial balance sheet is being drastically redrawn.

The reality of modern geopolitics is stark: material destruction on the front lines is mathematically symmetrical to surplus creation in selected corporate markets located thousands of miles away. There are clear corporate winners, losers experiencing real-time structural collapse, and a vast economic periphery silently footing the bill.

The Material Winners

The U.S. Defense Industry and the Dual Drivers of Demand

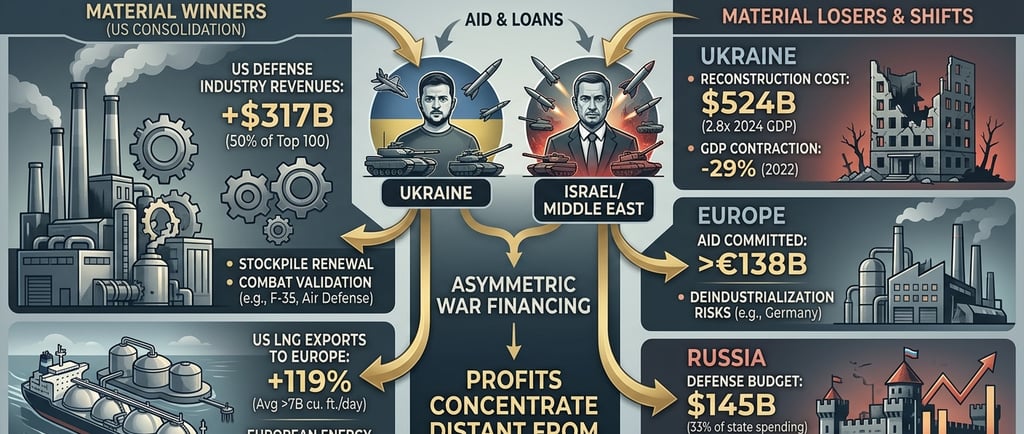

The maxim that the military-industrial complex thrives during periods of geopolitical instability has found its ultimate validation in the financial statements of 2022–2026, driven simultaneously by Kiev and Tel Aviv. According to data from the Stockholm International Peace Research Institute (SIPRI), the world’s top 100 defense companies generated $632 billion in revenue in 2023—a 4.2% real increase over the previous year. Of this total, the 41 corporations headquartered in the United States captured $317 billion, commanding exactly 50% of the entire global defense market.

Lockheed Martin led this surge, recording $60.8 billion in defense sales in 2023 and climbing to $63.9 billion in 2024. Giants such as RTX (formerly Raytheon), Northrop Grumman, and General Dynamics have been operating at maximum production capacity. While Ukraine triggered unprecedented demand for Javelin anti-tank missiles, HIMARS artillery systems, and 155mm ammunition, the conflict in Israel inflated the production of air defense interceptors (such as components for the Iron Dome and David's Sling systems), precision-guided munitions, and next-generation F-35 fighter jets.

The common driver of this growth is the acceleration of procurement contracts. When approving military aid packages, the U.S. government facilitates the drawdown of existing stockpiles under the banner of security assistance. This accounting mechanism ensures that multi-billion-dollar congressional appropriations are transformed into new, long-term procurement contracts with domestic defense contractors. The result is a continuous, publicly funded modernization of the U.S. military apparatus.

U.S. Liquefied Natural Gas (LNG) Exporters

On the energy security chessboard, the post-2022 shift represents one of the largest market transfers in modern history. Prior to the conflict, the Russian Federation held a virtual monopoly over Europe’s energy supply, providing more than 40% of the bloc's consumed natural gas through a network of low-cost pipelines. The abrupt cutoff of this supply and subsequent economic sanctions forced European nations to find immediate alternatives.

United States exporters of Liquefied Natural Gas (LNG) became the immediate beneficiaries of this crisis. U.S. LNG exports to the European market saw a meteorological 119% spike in 2022, reaching an average of over 7 billion cubic feet per day. By 2023, the U.S. consolidated its position as the world's largest LNG exporter, surpassing traditional competitors like Qatar and Australia.

This change of supplier came at an extraordinary cost to European buyers. The LNG transport model requires expensive liquefaction at the source, transport via specialized cryogenic vessels, and regasification at the destination, which drastically drove up European energy prices. During the peak of the crisis, Europeans paid up to five times the historical average of Russian pipeline gas, and roughly three to four times the domestic U.S. price (Henry Hub standard). American companies like Cheniere Energy operated with unprecedented profit margins, turning Europe's energy crisis into a multi-billion-dollar dividend for the Gulf Coast infrastructure sector.

Russia: The Short-Term Surprise Winner

The Russian economy displayed a paradoxical resilience that frustrated Western projections of an imminent financial collapse. Russia's federal revenue reached a record $320 billion in 2023. The Kremlin's survival mechanism relied on the strategic redirection of commodity export flows. Urals crude oil, banned from European ports and subject to the G7 price cap, was massively absorbed by new strategic buyers, namely India, China, and Turkey.

Operating through a "shadow fleet" of tankers and offering commercial discounts relative to Brent crude, Russia managed to keep its physical export volumes remarkably high. In April 2023, Russian oil exports peaked since the beginning of the invasion, recording 8.3 million barrels per day and generating a monthly cash flow of $15 billion. This capital influx, combined with heavy state stimulus into the domestic defense industry, allowed Russia's Gross Domestic Product (GDP) to grow by 4.1% in 2023 and 4.3% in 2024, outperforming most G7 economies in Western Europe.

However, the long-term balance sheet reveals severe structural cracks:

Russia's Economic Warning Signs (2025-2026) ├── Defense Budget: $145 billion for 2025 (33% of total state spending; >6% of GDP). ├── Growth Stagnation: Q1 2025 GDP growth collapsed to 1.4%, signaling industrial exhaustion. ├── Energy Revenue Decline: June 2025 oil & gas revenues hit their lowest level since Jan 2023. └── Frozen Assets: $300 billion in sovereign central bank assets remain frozen in Western banks.

The Material Losers

Europe: Paying the Highest Price Outside the War Zone

The European continent assumed the role of the primary financial shock absorber for the conflict on its borders, suffering deep impacts in both its fiscal sphere and its structural competitiveness. According to the Kiel Institute for the World Economy, European Union institutions and member states had committed over €138 billion in total assistance to Ukraine by February 2025, encompassing financial support, humanitarian aid, and military equipment.

Beyond direct fiscal outlays, Europe bore the economic brunt of a forced, accelerated energy transition. Replacing cheap Russian pipeline gas with imported LNG meant that European consumers and industries paid, on average, double the price for energy compared to their direct competitors in the United States. The epicenter of this shock was Germany, the bloc's largest economy. Historically dependent on cheap gas to power its chemical, steel, and automotive sectors, the country faced partial deindustrialization, recording consecutive quarters of technical recession and losing global market share to American and Chinese firms.

Eurozone inflation hit historic peaks between 2022 and 2023. As a long-term geopolitical response, the European Union instituted a new €150 billion integrated defense fund for rearmament and military standardization. While the crisis accelerated Europe's green transition—raising the share of renewables in the electricity mix from 37% in 2021 to 48% in 2025—the short- to medium-term cost to European industrial sustainability has been severe.

Ukraine: The Most Visible Material Destruction

For Ukraine, the conflict represents a scenario of unprecedented economic and demographic devastation in the 21st century. In the first year of the invasion (2022), the Ukrainian GDP suffered a brutal 29% contraction. Despite marginal stabilization later on, by 2024 the country's economic activity operated at just 78% of its pre-war levels.

A joint assessment by the UN, the World Bank, the European Union, and the Ukrainian government estimated the total accumulated cost for rebuilding national infrastructure at $524 billion—a figure representing 2.8 times Ukraine's projected 2024 GDP. The destruction heavily targeted the country's most critical assets, with the energy sector experiencing a 70% surge in cumulative damage over the course of 2024 alone.

The Ukrainian state has become entirely dependent on foreign financial lifelines to maintain basic governmental functions, such as paying public sector salaries and pensions. This support pipeline has been anchored by U.S. funding ($123 billion total mobilized through April 2025), the EU, and emergency credit programs from the International Monetary Fund (IMF). The extreme vulnerability of this financial architecture became clear in January 2025, when the incoming Trump administration cut 99% of direct U.S. military aid, exposing Kiev's budget to a deep and immediate fiscal deficit.

The United States: Winners Who Also Paid

United States participation in global conflict financing reveals a double-edged sword. On one hand, since 2022, Congress has approved an accumulated $175 billion in total assistance to Ukraine ($69.5 billion earmarked strictly for military supplies and $50.1 billion for direct budgetary support). Concurrently, billions of dollars have been routed to ensure Israel's operational readiness and ammunition replenishment in the Middle East.

Unlike purely financial aid, the vast majority of funds classified as military assistance never leave American soil in net terms. The capital remains in the U.S., flowing directly into the bank accounts of domestic defense corporations via new manufacturing contracts. This mechanism creates skilled jobs in key states, boosts manufacturing GDP, and acts as a domestic industrial policy disguised as foreign aid. Furthermore, the conflicts have reinforced the hegemonic role of the U.S. dollar as the exclusive settlement currency for major global defense contracts.

On the other hand, every billion dollars approved by the legislature expands the U.S. national debt, which is already at historic highs. This fiscal cost has become a central weapon in domestic political rhetoric. The narrative that American taxpayers are uniquely footing the bill for global security was heavily leveraged to justify an isolationist foreign policy pivot in early 2025, despite analytical data showing that European institutions have committed more total financial capital to the Ukraine crisis than the U.S.

The Legacy Military Playbook: Stockpile Renewal and Real-World Testing

The delivery of military aid to Ukraine and the supply dynamics in the Middle East operate under a logistics and accounting engine vital to defense economics: the cycle of planned obsolescence and real-world combat validation.

A significant portion of the arms hardware sent to Kiev by NATO members consisted of legacy equipment engineered late in the Cold War. Systems like early-generation Leopard tanks, M113 armored personnel carriers, and older M2 Bradley fighting vehicles would have soon required expensive decommissioning, ecological disposal, or deep structural overhauls funded entirely by domestic taxpayers. By transferring these assets to the Ukrainian front, Western governments eliminate long-term storage liabilities and clear the fiscal runway to justify new, multi-billion-dollar budgets for next-generation replacements, such as F-35 fighter jets or advanced artillery systems.

The Live-Combat Laboratory: In the case of Israel, the conflict acts as a high-tech laboratory in real time. The intensive use of smart systems, artificial intelligence algorithms for target selection, and advanced ballistic missile interceptors provides American and Israeli defense firms with performance data that no computer simulation can replicate.

The battle-testing of these systems drives up the global market value of the proprietary technology and attracts new state buyers, turning regional conflict into a high-value technological showroom.

Conversely, Moscow has pivoted its manufacturing base toward total mobilization, expanding domestic production of standard 152mm artillery shells by an astonishing 420%, according to SIPRI. While this hypertrophy sustained the war effort and generated a short-term manufacturing employment boom, it has created a dangerous, structural macroeconomic dependency for Russia's post-2025 future.

Conclusion · The Real Global Balance Sheet

I think that an objective analysis of financial data from 2022 to 2026 demonstrates that contemporary conflicts operate as massive macroeconomic vacuum pumps. They drain public capital from taxpayers and civilian energy savings, concentrating those funds into the net revenues of strategic defense and infrastructure energy sectors.

The territories directly caught in the crossfire face a bleak post-conflict horizon marked by fractured social fabrics, compromised industrial capacity, and massive reconstruction liabilities—best exemplified by the $524 billion required for Ukraine. Europe has paid the material price for its geopolitical independence through partial deindustrialization and structurally higher energy costs. The United States has consolidated its industrial and energy dominance, though at the cost of deep domestic political polarization and a rising national debt. Russia and mobilized regional powers face the daunting challenge of sustaining economies warped by war budgets that stifle long-term civilian development.

Regardless of how frozen sovereign assets are liquidated or transferred in the future, the primary macroeconomic lesson of modern warfare remains unchanged: the real profits of war rarely stay where the bombs fall. Instead, they accumulate in the balance sheets of those who own the infrastructure of production and stand strategically furthest from the trenches.

Selected Bibliography

Stockholm International Peace Research Institute (SIPRI). Trends in International Arms Transfers and Global Defense Spending: 2023–2025. (2026).

Kiel Institute for the World Economy. Ukraine Support Tracker: Financial and Military Commitments to the War Effort. (2026).

International Monetary Fund (IMF). Geopolitical Fragmentation and the Global Energy Trade: Economic Shocks and Resilience. (2026).

U.S. Congressional Budget Office (CBO). Fiscal Impact of Foreign Military Assistance and Defense Procurement Appropriations. (2025).

OECD. Economic Outlook: The Cumulative Cost of Conflict on Global GDP (2022–2026). (2026).

Bloomberg Intelligence. Defense & Energy: The Industrial Winners of Geopolitical Volatility. (2026).

United Nations & World Bank. Ukraine: Third Rapid Damage and Needs Assessment (RDNA3). (2025).

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy