The Definitive Guide to Crypto Cards in 2026

Global comparative analysis and market trends

CREDIT CARD

By Marcelo Salamon

7/12/20267 min read

Abstract

The market for payment methods integrated with digital assets has consolidated as a cornerstone of the digital economy in 2026. This article analyzes the fundamental criteria for choosing cryptocurrency cards, establishing a detailed comparison among the leading global solutions (Coinbase, Crypto.com, KAST, Nexo, Bybit, among others). Focusing primarily on the United States market while extending the analysis to Europe and Latin America, this study examines variables such as regulatory compliance (KYC), fee structures, stablecoin support, and regional usability by specific countries. The objective is to provide an analytical guide for different user profiles seeking efficiency in converting and spending digital assets within the traditional retail ecosystem.

Introduction

The convergence between Traditional Finance (TradFi) and crypto assets has evolved from a technological promise into an everyday operational reality in 2026. While in the past decade utilizing digital currencies for day-to-day purchases required complex settlement processes and transfers to traditional bank accounts, the maturity of major payment networks (specifically Visa and Mastercard) and international regulatory advancements have transformed crypto cards into mainstream financial tools.

Today's infrastructure allows digital asset holders to transact at millions of commercial establishments worldwide with the same speed and convenience as a conventional debit or credit card. The real-time clearing mechanism at the point of sale has resolved the industry's primary logistical bottleneck: the merchant receives local fiat currency (such as US Dollars or Euros), while the user's balance is debited directly from their digital assets or stablecoins.

However, the geographic expansion of this market has created a fragmented landscape. Users residing in the United States, the European Union, or Latin America face completely distinct regulatory realities, transaction costs (spreads), and product availability.

This article provides an in-depth, structured analysis of the current market leaders. We evaluate the practical viability of these financial tools under a rigorous matrix of criteria, mapping out the industry frontrunners and the best alternatives for each macroeconomic user profile.

Fundamental Criteria for Analysis

To evaluate the efficiency of a crypto card, simply looking at the payment network logo is insufficient. In a globalized and highly regulated economic landscape, we establish over twenty critical audit parameters, divided into four major pillars:

Geographic Reach and Accessibility

Detailed Regional Availability: The legal and logistical capability of the issuer to operate in specific jurisdictions, issuing physical plastic or virtual credentials valid for residents of particular countries.

Onboarding for International Users: Entry barriers for users outside the issuer's primary region, including support for local deposits, native-language customer support, and the bureaucracy of opening an account from an external tax residence.

KYC (Know Your Customer) Process: The mandate and rigor of identity verification, which is a crucial factor for user legal compliance under financial regulatory bodies.

Technical and Network Infrastructure

Payment Network and Integration: Seamless integration with Visa or Mastercard digital networks and immediate compatibility with mobile contactless wallets (Apple Pay and Google Pay).

Issuance Format: Availability of physical cards (essential for ATM cash withdrawals and backup) and virtual cards (focused on e-commerce security).

Custody Flexibility: Support for low-volatility assets (stablecoins such as USDC, USDT, EURC) and blue-chip crypto assets (BTC, ETH, SOL, XRP, AVAX).

Financial Dynamics and Operational Costs

Deposit Mechanisms: Support for native blockchain transfers or traditional banking rails such as ACH/Wire (US), SEPA (Europe), and PIX (Brazil).

Exchange Efficiency: Hidden costs represented by the conversion spread, alongside upfront issuance or monthly maintenance fees.

Incentive Structure: Crypto-back reward programs, tier-based loyalty benefits, and daily/monthly spending and withdrawal limits.

Security and Corporate Support

Auditing of anti-fraud security protocols, responsiveness of customer support channels, and the institutional solvency of the issuing company.

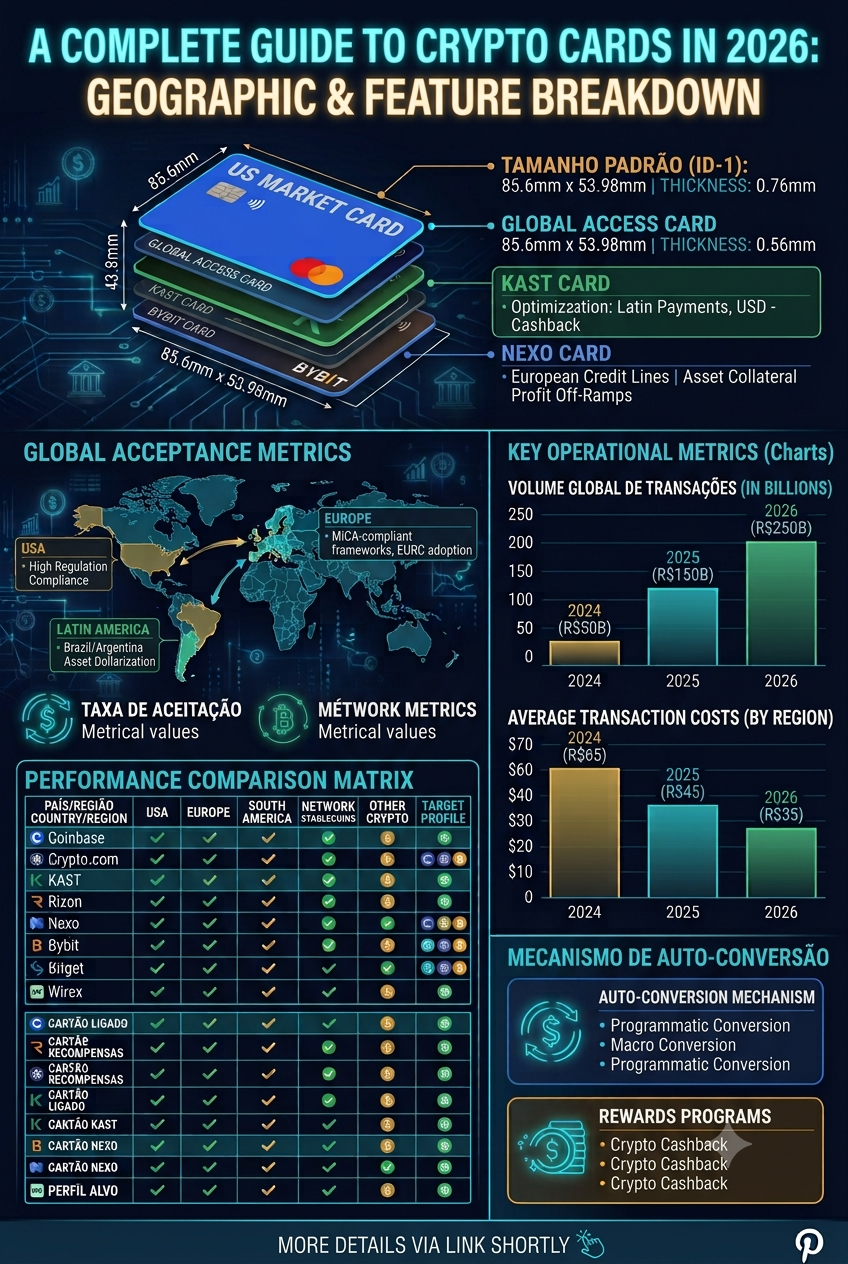

Regional Market Landscapes and Country-Specific Acceptance

INTELLIGENCE MARKET MATRIX

| Region / Key Countries | Core Operational Characteristic |

| US (All 50 States) | SEC/FinCEN compliance, strict capital gains |

| Europe (EEA, UK, Switzerland | MiCA-compliant frameworks, EURC adoption |

| Latin America (Brazil, Argentina) | Inflation hedge, synthetic USD monetization |

The Primary Focus: The United States Market

The US represents the most mature yet highly complex market from a securities regulation and tax compliance perspective. Cards operating on American soil require strict KYC and are deeply integrated with tax reporting frameworks to calculate capital gains at the exact moment of asset conversion.

Domestic acceptance spans all 50 states, though stringent local regulations (such as New York State's BitLicense framework) can restrict certain issuers. The average American user prefers seamless integration with existing regulated exchanges (like Coinbase and Gemini) or solutions focused strictly on digital US dollars to mitigate daily volatility risks.

The European Market

Europe stands out for its regulatory clarity, driven by the comprehensive implementation of MiCA (Markets in Crypto-Assets) rules. Card issuance and acceptance extend across the entire European Economic Area (EEA)—including economic powerhouses like Germany, France, Italy, and Spain—as well as the United Kingdom and Switzerland via local financial arrangements.

The adoption of cards featuring direct conversion of Euro-pegged stablecoins (EURC) has grown significantly. Established payment providers find the region to be a welcoming ecosystem for issuing hybrid debit and credit cards, heavily backed by the Eurozone's instant settlement infrastructure.

The Latin American Scenario

In Latin America, product offering and account validation are heavily concentrated in Brazil and Argentina, followed by Colombia, Chile, and Mexico. In these markets, crypto cards serve a distinct macroeconomic purpose: wealth preservation and access to synthetic dollarization. The utilization of US Dollar-pegged stablecoins (USDT and USDC) has transformed into a viable alternative to traditional international bank accounts. The primary competitive advantage in the region, particularly in Brazil, is direct integration with instant local payment networks (like PIX), enabling real-time deposits and fiat liquidations.

Detailed Analysis and Acceptance Scope of Leading Cards

Based on our established comparative matrix, we evaluate the market positioning, technical features, and precise geographic reach of each major issuer:

Coinbase Card

Issuance and Availability: Available to legal residents across the United States (subject to minor state-level variations based on local virtual asset licensing). It is not available for direct issuance to residents of Brazil or most of South America.

Payment Network: Visa.

Operational Analysis: The default choice for US-based retail crypto users. Because it links directly to accounts on the largest US-regulated exchange, it eliminates transfer friction. The KYC process is stringent. The card offers automatic conversion of USDC without predatory transaction fees, making it highly efficient for everyday domestic retail spending. It features full Apple Pay and Google Pay integration.

Crypto.com Visa

Issuance and Availability: One of the most globally accessible ecosystems. It is actively issued to residents in the United States, Canada, all European Economic Area (EEA) nations (Germany, France, etc.), the United Kingdom, and features native, direct local issuance in Brazil, streamlining KYC for South American users with domestic documentation.

Payment Network: Visa.

Operational Analysis: Historically renowned for its aggressive incentive and rewards structure. The platform requires staking its native token (CRO) to unlock premium crypto-back tiers and travel perks (such as international airport lounge access). Supporting a massive array of stablecoins and altcoins, it is ideal for investors looking to maximize yield on global expenditures.

KAST

Issuance and Availability: Purpose-built for cross-border financial corridors. It supports account opening and issuance for residents of the United States and several Latin American countries, including robust onboarding support for Brazil.

Payment Network: Visa.

Operational Analysis: A rapidly growing player among users leveraging digital dollar ecosystems for cross-border transactions. Focused on optimizing USDC and USDT conversions, KAST removes traditional banking complexities for international users, offering a direct bridge between high-speed blockchains and legacy point-of-sale terminals. It is heavily utilized by remote professionals receiving foreign income and spending locally.

Rizon Visa

Issuance and Availability: Geographically streamlined and optimized for the North American market (United States). Its domestic remittance and payment services target corporate and personal settlement simplicity within US territories.

Payment Network: Visa.

Operational Analysis: Designed specifically for the circulation and spending of dollar-denominated stablecoins. Its core appeal lies in predictability: users know their exact digital purchasing power without daily exposure to the price volatility of Bitcoin or Ethereum. It serves as a highly efficient, low-spread transactional tool.

Nexo Card

Issuance and Availability: Available to residents of the European Economic Area (EEA) and the United Kingdom. Countries such as Germany, Spain, Portugal, and France have full operational support. It does not offer direct card issuance to tax residents in the United States (due to regulatory restrictions on interest-bearing/credit products) or South America.

Payment Network: Mastercard.

Operational Analysis: Features an innovative dynamic by functioning under a Crypto-Backed Credit Line model. Instead of selling the user's assets at the moment of purchase—which triggers a taxable event in most European jurisdictions—Nexo opens an instant credit line using the deposited crypto as collateral. The user retains long-term asset ownership while accessing immediate liquidity for consumption.

Bybit Card

Issuance and Availability: Broad international account acceptance, with card issuance available across the United Kingdom, the EEA, and experiencing strong market traction in South America, including active support for the Brazilian market.

Payment Network: Mastercard.

Operational Analysis: Deeply integrated into the Bybit trading platform. It is the ideal tool for active traders who need to quickly liquidate trading profits to cover real-world expenses, featuring highly competitive conversion rates within the global exchange market.

Bitget Card

Issuance and Availability: Expansion efforts are strategically aimed at emerging markets. It holds strong penetration across South America (specifically Brazil and Argentina) and select regions in Asia. It does not issue to the United States due to FinCEN/SEC compliance barriers.

Payment Network: Visa / Mastercard (depending on the specific sub-region and issuance batch).

Operational Analysis: Mirroring the exchange-linked model, it focuses on the instant conversion of trading account balances. It enjoys high adoption in Latin America due to localized incentive campaigns, fully translated interfaces, and seamless USDT collateral clearing via regional fiat payment gateways.

Wirex

Issuance and Availability: Deeply anchored in its historic core markets of the United Kingdom and the European Union (France, Italy, Ireland, Portugal, among others). While it has engaged in broader global partnerships in the past, its core card issuance operations remain centered within the European regulatory framework.

Payment Network: Visa.

Operational Analysis: One of the sector's pioneers in Europe, Wirex has consolidated its position by offering native multi-currency accounts. It allows users to toggle seamlessly between traditional fiat accounts (such as Euros and British Pounds) and classic crypto wallets, maintaining a user experience closely resembling a traditional digital neobank.

Conclusion

The crypto card market has achieved functional maturity. Far from being niche products for tech enthusiasts, these tools operate as vital gears for global financial efficiency in 2026.

Choosing the ideal card does not depend solely on nominal rewards (like cashback percentages) but rather on the geography, nationality, and tax profile of the user:

For residents of the United States, strict regulatory compliance, ease of tax reporting, and the stability of domestic ecosystems like Coinbase or localized credit structures remain paramount.

In Europe (the EU and the UK), intelligent credit models that preserve long-term wealth without triggering immediate asset liquidations, such as Nexo, drive the pace of innovation.

In Latin America, particularly within Brazil's highly connected ecosystem, solutions that merge local instant payment rails with global stablecoin liquidity bridge critical gaps left by traditional legacy banking systems.

The trend moving forward points toward a further reduction in conversion spreads and a complete fusion between traditional fiat bank accounts and decentralized Web3 wallets.

References

COINBASE INC. The State of Crypto Report 2026: Institutional and Retail Integration in Payment Systems. San Francisco, 2026.

CRYPTO.COM RESEARCH. Global Crypto Adoption Index and Payment Card Evolution. Singapore, 2025.

EUROPEAN CENTRAL BANK (ECB). Markets in Crypto-Assets (MiCA) Regulation Impact on Retail Payment Instruments. Frankfurt, 2025.

FINANCIAL CRIMES ENFORCEMENT NETWORK (FinCEN). Regulatory Framework for Convertible Virtual Currencies and Prepaid Card Programs. Washington, D.C., 2024.

VISA & MASTERCARD NETWORKS. Digital Assets and the Evolution of Merchant Settlement Infrastructure. New York, 2025.

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy