The Palantir Valuation Paradox

Can its enterprise AI engine sustain the second-half rally in 2026?

INVESTIMENT

By Marcelo Salamon

7/5/20269 min read

Abstract

This report analyzes the financial and operational trajectory of Palantir Technologies Inc. (NASDAQ: PLTR), evaluating its strategic positioning in the transition from experimental Artificial Intelligence (AI) to enterprise and defense operational AI. We investigate the recent market correction that compressed the company’s market capitalization from its peak of over $400 billion in late 2025 to its current range of $309 billion to $315 billion as of July 2026, with shares trading at $129.30. In light of historic first-quarter results for 2026—featuring revenue growth of 85% year-over-year and a stretched Price-to-Earnings (P/E) multiple of 145x—this study projects stock valuation scenarios through the end of the fiscal year, weighing the acceleration of the Artificial Intelligence Platform (AIP) against the risks of multiple compression and geopolitical concentration.

Keywords: Palantir Technologies; Operational Artificial Intelligence; Stock Valuation; NASDAQ: PLTR; Corporate Finance; Defense Technology.

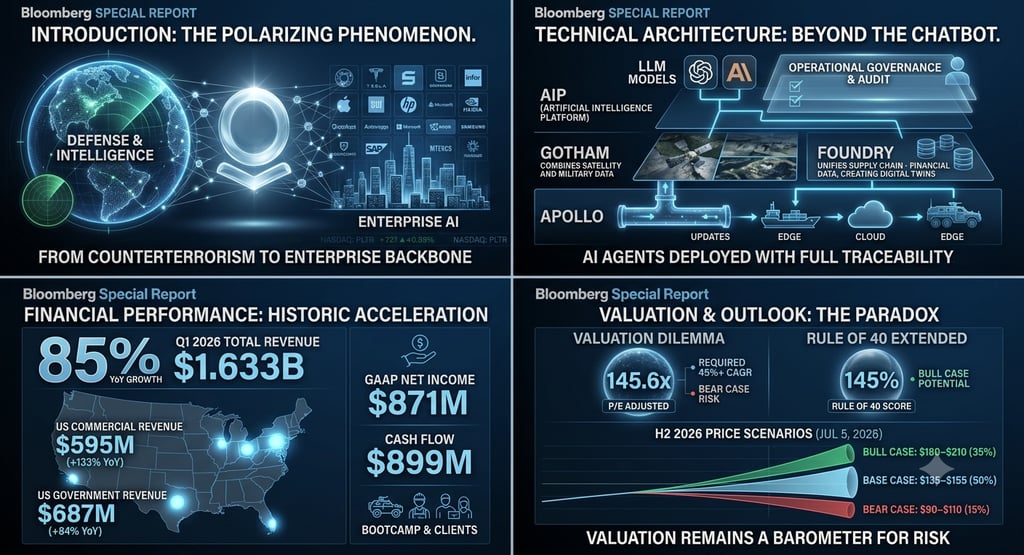

Introduction: Wall Street’s Most Polarizing Phenomenon

Few companies in the global technology ecosystem ignite debates as fierce across hedge fund trading desks and equity research departments as Palantir Technologies Inc. Founded in 2003 with seed capital from In-Q-Tel, the CIA's venture capital arm, and conceptualized by prominent Silicon Valley figures including Peter Thiel, Stephen Cohen, Joe Lonsdale, Nathan Gettings, and its eccentric CEO, Alex Karp, the company has emerged from the obscurity of counterterrorism operations to become a backbone of modern AI infrastructure.

Named after the seeing-stones in J.R.R. Tolkien’s lore, Palantir’s original promise—to decrypt the invisible by connecting massive, disparate datasets—reached its commercial zenith in 2023 with the launch of its Artificial Intelligence Platform (AIP). What followed was one of the largest equity rallies of the decade, culminating in a market capitalization that temporarily surpassed $400 billion at the close of 2025.

However, market dynamics in 2026 have imposed a more sober reality. After hitting an all-time high of $207.52, PLTR shares underwent a severe correction of approximately 37.7%, touching a floor of $106.37 in June before regaining momentum to trade in the current $129.30 range in early July 2026. This price volatility highlights the core dilemma facing investors: Is Palantir an unparalleled, cash-generating growth engine or an overhyped tech stock trading at unsustainable multiples? This report breaks down its product mechanics, its latest financial statements, and quantitative models to outline valuation perspectives for the remainder of the year.

Chart 1: Recent Trajectory of PLTR Stock (2025-2026) $207.52 (All-Time High - Nov 2025) \ \

$129.30 (Current Price - July 2026) \ /

\ / $106.37 (Correction Floor - June 2026)

Technical Architecture: Moving Beyond Chatbots to Autonomous AI Agents

To understand the resilience of Palantir’s business model, one must separate it from traditional Software-as-a-Service (SaaS) companies or generic Large Language Model (LLM) providers. The company does not sell abstract AI intellectual property; it provides the operational fabric that allows large organizations to deploy algorithms within chaotic data environments. Its revenue engine is built upon four analytical pillars:

Palantir Gotham

The company’s flagship platform, focused primarily on governments, military branches, and Western intelligence agencies. Gotham integrates highly heterogeneous structured and unstructured data—including satellite feeds, geospatial sensors, signal intelligence intercepts, and military logistics reports—converting them into a unified operational map. It is the core tool that cemented Palantir’s reputation within the Pentagon, actively supporting national security logistics for the US and its NATO allies.

Palantir Foundry

Launched to translate the company's governmental expertise into the large-scale corporate environment. Foundry acts as a central operating system for the private sector, interconnecting legacy ERP systems, isolated financial spreadsheets, and complex supply chain data. Corporations in energy, advanced manufacturing, healthcare, and aviation use the platform to create "digital twins" of their operations, enabling real-time stress testing and margin optimization.

Palantir Apollo

The infrastructure layer that solves a major bottleneck in modern software engineering: continuous deployment and application management. Apollo works autonomously to ensure that both Gotham and Foundry receive critical security and algorithmic updates across any computing environment. This ranges from public cloud architectures (AWS, Azure) to edge computing platforms installed on submarines, warships, or remote refineries operating without stable internet connectivity.

AIP (Artificial Intelligence Platform)

Introduced in mid-2023, AIP has become the primary driver of the company’s accelerating revenue. Unlike platforms focused purely on conversational interfaces, AIP connects proprietary and third-party LLMs (such as those from OpenAI and Anthropic) directly to an organization’s secure, operational data. The competitive advantage lies in its guardrails: AIP offers full traceability and audit logs for every decision made by autonomous AI agents. If an agent alters a supply chain order or re-routes a logistical path, the platform maps the underlying rationale in compliance with corporate security rules, mitigating legal risks and algorithmic hallucinations.

Financial Performance: Historic Acceleration in Q1 2026

Audited financial results for the first quarter of 2026, reported in May, demonstrated that management's growth thesis is backed by aggressive market share expansion in the North American market.

Palantir’s total revenue expanded to $1.633 billion for the quarter, representing robust growth of 85% year-over-year. This metric marked the most significant quarterly acceleration since the company's September 2020 direct listing on the New York Stock Exchange.

Total Revenue: $1.633 billion (+85% YoY growth) — Highest advance since Direct Listing.

Total US Revenue: $1.282 billion (+104% YoY growth) — Accounts for 79% of global revenue.

US Commercial Revenue: $595 million (+133% YoY growth) — Private sector hyper-expansion.

US Government Revenue: $687 million (+84% YoY growth) — Driven by Defense and NATO demands.

GAAP Net Income: $871 million (+307% YoY growth) — 53.3% GAAP net margin.

Cash Flow from Operations: $899 million — Key liquidity factor; total cash position stands at $8.0 billion.

The commercial strategy of deploying AIP "bootcamps"—where Palantir engineers build real operational workflows for enterprise clients in a matter of days—has directly translated into high-value contract conversions. During the first quarter of 2026, the company closed a record volume of 206 individual contracts valued at over $1 million, including 72 deals above $5 million and 47 surpassing the $10 million threshold. Total Contract Value (TCV) closed during the quarter reached $2.41 billion, up 61% year-over-year.

Business scalability was reflected in efficiency margins, with the adjusted operating margin hitting 60% ($984 million). This allowed leadership to raise its full-year guidance significantly. Management now projects that consolidated revenue for the fiscal year 2026 will land between $7.650 billion and $7.662 billion, representing a 71% annualized expansion.

The Valuation Dilemma: Multiples versus Earnings Execution

Despite flawless operational performance and an immaculate balance sheet—free of debt and boasting $8.0 billion in cash, cash equivalents, and US Treasuries—Palantir’s equity pricing remains a major point of divergence in discounted cash flow (DCF) models across investment banks.

With the stock trading at $129.30, the company’s forward adjusted P/E multiple sits at approximately 145.6x. When analyzing the Enterprise Value to Forward Revenue (EV/Sales) metric, the indicator hovers around 39.3x for the full year 2026. This level of valuation demands near-flawless operational execution over the next 36 months.

Comparative Valuation Multiples (July 2026) ------------------------------------------------------- Palantir (PLTR) Forward P/E: ██████████████████ 145.6x Software Sector Average: ███ 28.5x -------------------------------------------------------

Market bears point out that multiples of this caliber historically precede periods of stagnation or severe corrections if any macroeconomic slowdown occurs. To justify a 145x P/L, Palantir needs to not only meet its aggressive 71% growth guidance for 2026 but maintain a compound annual growth rate (CAGR) exceeding 45% through the end of the decade.

Conversely, bulls argue that Palantir operates under the dynamics of a hyper-extended "Rule of 40"—a software industry metric that combines revenue growth rate and profit margin. In Q1 2026, Palantir’s combined score reached an extraordinary 145% (85% revenue growth plus a 60% adjusted operating margin), a profile virtually unique among large-cap companies in the S&P 500.

Valuation Outlook for the Remainder of the Year: Three Market Scenarios

Palantir shares will serve as a key barometer for global tech risk appetite in the second half of 2026. Price action will be governed by the company's ability to sustain private-sector commercial expansion without suffering multiple compression in a potentially restrictive US interest rate environment. Below, Bloomberg Intelligence outlines three probabilistic scenarios for the asset through December 2026.

Bull Case: Price Target Between $180 and $210

Assigned Probability: 35%

In this scenario, Palantir outperforms the ceiling of its revised annual guidance, delivering revenues close to $7.8 billion for 2026. This upside is catalyzed by widespread enterprise adoption of AIP in European and Asian markets, where current penetration remains modest compared to its 79% concentration in the US.

From a macro perspective, the materialization of large-scale, multi-year military contracts—such as the execution of the estimated $10 billion, ten-year contract with the US Army and new demands for "Sovereign AI" in partnership with NVIDIA for NATO allies—acts as an institutional catalyst. With earnings beating consensus and the Rule of 40 score remaining above 120%, the market accepts the premium multiple. PLTR stock would retest its all-time highs, supported by target upgrades from firms like Bank of America Securities, which maintains a price target of $255.

Base Case: Price Target Between $135 and $155

Assigned Probability: 50%

This represents the most likely analytical equilibrium. The company delivers exactly on its revised May guidance: revenue in the $7.65 billion range and US commercial growth exceeding 120%. The current pricing of $129.30 has already absorbed a significant portion of the risk premium following the 37% correction from all-time highs.

Under this framework, investment firms like Morgan Stanley (price target: $205) and Mizuho (price target: $185) maintain their neutral or moderate outperform stances, acknowledging that the stock has "grown into its valuation." The equity undergoes institutional accumulation in the $140 range, moving up gradually as subsequent Q2 and Q3 2026 earnings reports confirm sustainable GAAP margin expansion and steady free cash flow generation (projected at approximately $4.3 billion adjusted for the full year).

Bear Case: Price Target Between $90 and $110

Assigned Probability: 15%

The downside thesis rests on sharp multiple compression triggered by two factors: a temporary saturation of the North American enterprise market for large-scale AI solutions and competitive advancements by foundational model creators. If companies like OpenAI, Anthropic, and Alphabet successfully move deeper into the operational framework layer for corporate decision-making, Palantir could lose its monopoly on the "AI with corporate governance" narrative.

Additionally, any signs that second-half revenue growth is slowing to double-digit rates below 50% YoY would trigger automated sell programs by quantitative funds. As noted by the equity research team at RBC Capital, whose bear-case target sits at $90, a reduction in the pace of government contract procurement due to budgetary delays or policy shifts would strip the stock of its valuation premium, pushing it back to double-digit technical support levels.

Critical Risk Factors and Competitive Dynamics

Evaluating an investment in Palantir for the remainder of 2026 requires monitoring three critical risk vectors:

Geographic Concentration and US Macro Dependency

While a 133% expansion in the US private sector highlights commercial momentum, the fact that the domestic market accounts for 79% of total revenue exposes Palantir to geographic concentration risks. International growth has faced steeper cultural barriers and more rigid data governance frameworks, notably through regulatory scrutiny under the European Union's AI Act. If the US economy experiences a slowdown in corporate spending during the second half of 2026, Palantir may find it difficult to offset that drag via other regions.

Political and Budgetary Volatility in Government Contracts

Defense and intelligence procurement cycles are inherently volatile and subject to political shifts and public oversight. Palantir's explicit positioning in defense of Western geopolitical interests—a stance frequently championed by CEO Alex Karp at global forums—solidifies its position within the Pentagon but may limit its addressable market (TAM) in emerging economies or non-aligned nations.

Share Dilution from Stock-Based Compensation (SBC)

Historically, a core concern for minority shareholders has been the substantial volume of Stock-Based Compensation (SBC) issued by the company. In Q1 2026, Palantir reported an expense of $201.5 million under this line item. Although this dilution is currently offset by exponential GAAP net income growth ($871 million), investors should monitor whether the pace of equity issuance to retain engineering talent pressures earnings per share (EPS) if revenue growth stabilizes.

Conclusion: The Line Between Technological Value and Capital Risk

Palantir Technologies enters the second half of 2026 as a unique entity on Wall Street. The historic quarter reported in May proved that the company possesses the right infrastructure at the right macroeconomic moment: the global shift away from generative AI experimentation toward enterprise-wide automation. The AIP platform has established itself as a highly effective enterprise conversion tool, as evidenced by three-digit corporate growth in the US market.

However, for investors evaluating capital allocation through the end of fiscal year 2026, the primary challenge is not the quality of the software developed by Karp and his team, but the mathematical reality of its valuation. Trading at $129.30 with a forward adjusted P/E multiple above 145x, PLTR shares leave little room for operational friction.

The base case suggests a path of moderate, sustained appreciation through year-end, with the stock stabilizing between $135 and $155 as large institutional houses recalibrate their earnings estimates. Palantir has transitioned from a highly speculative retail favorite into a core infrastructure component of the S&P 500. Investors allocating capital at these levels must accept the inherent volatility of an asset whose valuation is tied to the transformation of decision-making frameworks across the world’s largest corporations and defense establishments.

Bibliography

BANK OF AMERICA GLOBAL RESEARCH. Palantir Technologies: AIP Bootcamps Trigger Unprecedented Enterprise Adoption Pipeline. New York: BofA Securities Equity Research, June 2026.

BLOOMBERG INTELLIGENCE. Software and IT Services Quarterly Outlook: Navigating Extreme Valuation Multiples in the Era of Autonomous AI Agents. New York: Bloomberg L.P., July 2026.

INDMONEY INVESTMENT ANALYSIS. Why Palantir Stock Fell: PLTR Crash & Recovery Explained - AI Valuation Analysis. July 2026. Available at: https://www.indmoney.com/blog/us-stocks/palantir-stock-crash-pltr-recovery-explained-ai-valuation-analysis. Accessed: July 5, 2026.

MORGAN STANLEY RESEARCH. The Valuation Paradox: Assessing Risk-Reward Frameworks for High-Growth AI Infrastructure Stocks. New York: Morgan Stanley & Co. LLC, May 2026.

PALANTIR TECHNOLOGIES INC. Palantir Reports Q1 2026 U.S. Revenue Growth of 104% Y/Y and Revenue Growth of 85% Y/Y; Raises FY 2026 Revenue Guidance to 71% Y/Y Growth. Denver: Palantir Investor Relations, May 4, 2026. Available at: https://investors.palantir.com/. Accessed: July 5, 2026.

QUARTZ MEDIA. Palantir Q1 2026 earnings: revenue surges 85%, guidance raised. Bloomberg / Getty Images, Updated May 4, 2026. Available at: https://qz.com/palantir-q1-2026-earnings-revenue-growth-guidance-050426. Accessed: July 5, 2026.

TIKR FINANCIAL. Palantir Stock Rallies as DA Davidson Upgrades on Attractive Valuation. TIKR Blog, July 3, 2026. Available at: https://www.tikr.com/blog/pltr-palantir-nasdaq-stock-rallies-3-7-as-da-davidson-upgrades-on-attractive-valuation. Accessed: July 5, 2026.

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy