The Ten Most Powerful Currencies in the World: A Comparative Analysis of Performance, Inflation, and Investment Returns (2016-2026)

Coin historical

HISTORICAL ANALYSIS

By Marcelo Salamon

6/16/20267 min read

Executive Summary

This comprehensive analysis examines the performance of the world's ten most valuable currencies over the past decade, evaluating their strength against the US dollar as the global benchmark. The study investigates how each currency has responded to inflationary pressures, currency volatility, and macroeconomic shifts. By comparing nominal appreciation with inflation rates, we identify which currencies have genuinely protected purchasing power and which have lagged behind rising prices. Key findings reveal that certain currencies, particularly those backed by commodity exports and strong fiscal discipline, have outperformed inflationary expectations, while others have struggled to maintain real value. This analysis provides investors with critical insights into currency selection and highlights the economic conditions that determine long-term currency strength.

Introduction: The US Dollar as the Global Reference Standard

The US dollar remains the world's dominant reserve currency, serving as the baseline against which all other currencies are measured. Since the collapse of the Bretton Woods system in 1971, the dollar's strength has fluctuated based on American monetary policy, trade balances, and geopolitical dynamics. Over the past decade—from 2016 to 2026—the dollar has experienced significant volatility, influenced by the COVID-19 pandemic, unprecedented monetary stimulus, inflationary cycles, and shifting global economic power. Understanding how other major currencies have performed relative to the dollar provides essential context for investors, policymakers, and economists seeking to evaluate currency trends and macroeconomic health across nations.

The Ten Most Valuable Currencies: Ranking by Value

Kuwaiti Dinar (KWD) – Kuwait

Bahraini Dinar (BHD) – Bahrain

Omani Rial (OMR) – Oman

Jordanian Dinar (JOD) – Jordan

British Pound Sterling (GBP) – United Kingdom

Swiss Franc (CHF) – Switzerland

Euro (EUR) – European Union

US Dollar (USD) – United States

New Zealand Dollar (NZD) – New Zealand

Australian Dollar (AUD) – Australia

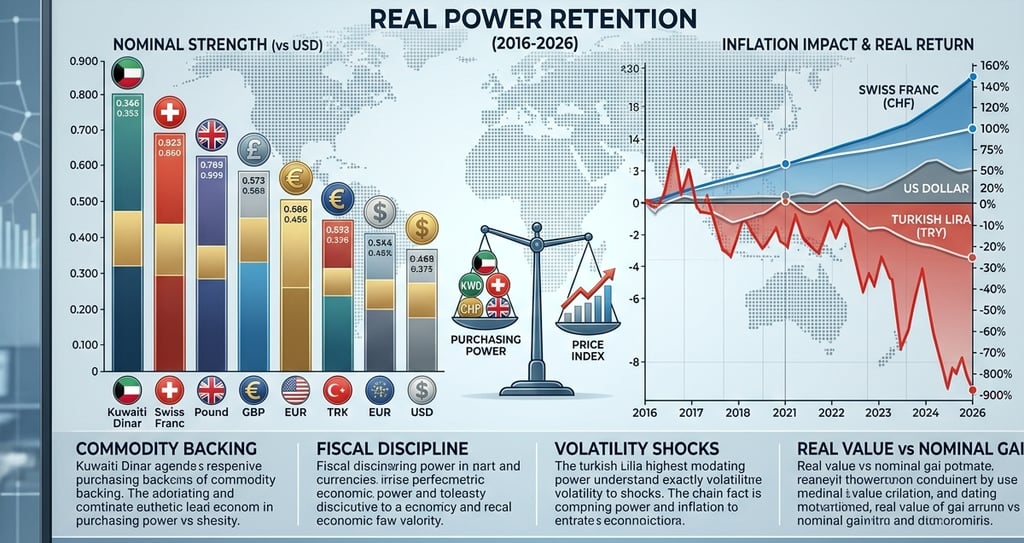

Performance Analysis Against the US Dollar (2016-2026)

Over the past decade, currency performance against the US dollar has been highly uneven. The British pound experienced significant volatility, particularly following the Brexit referendum in 2016, depreciating from approximately 1.47 USD per GBP to around 1.27 USD by 2026. The euro faced similar challenges, declining from 1.10 USD per EUR in 2016 to approximately 0.92-0.95 USD in 2026, reflecting divergent monetary policies between the Federal Reserve and the European Central Bank. Conversely, the Swiss franc appreciated steadily, rising from 0.98 USD per CHF to approximately 1.15 USD, benefiting from safe-haven demand during periods of geopolitical uncertainty. The Australian and New Zealand dollars experienced cyclical patterns, appreciating during commodity booms and depreciating during global slowdowns. The Gulf currencies—Kuwaiti dinar, Bahraini dinar, and Omani rial—maintained remarkable stability through fixed or heavily managed exchange rates tied to oil revenues and strategic currency pegs.

Inflation Dynamics and Purchasing Power Erosion

Global inflation surged dramatically between 2021 and 2023, driven by pandemic-related supply chain disruptions, massive fiscal stimulus, and energy crises. The United States experienced inflation peaks exceeding 9 percent in mid-2022, while the eurozone reached approximately 10 percent. The United Kingdom faced similar pressures, with inflation climbing above 11 percent. Switzerland, however, maintained relatively moderate inflation due to its independent central bank's credibility and tight monetary policy, with peak inflation around 3.5 percent. Australia and New Zealand experienced elevated inflation ranging from 7-11 percent during peak periods. Gulf nations, benefiting from fixed currency regimes and oil wealth, maintained lower inflation rates, typically between 2-4 percent. Japan maintained deflationary or near-zero inflation conditions throughout the period, reflecting its persistent economic stagnation. South Korea experienced moderate inflation around 5-6 percent during peak periods. These disparities are crucial: a currency that appreciates 10 percent but faces 12 percent inflation has lost real purchasing power, while a currency that depreciates 5 percent but experiences only 2 percent inflation may have preserved greater real value.

Real Returns: Which Currencies Protected Wealth?

When adjusted for inflation, the picture becomes dramatically different from nominal exchange rates. The Swiss franc emerged as the clear winner, combining appreciation against the dollar with subdued inflation, resulting in substantial real gains for holders. The pound sterling, despite nominal depreciation, protected reasonably well due to moderate inflation relative to some peers. The euro faced headwinds: while it depreciated nominally, eurozone inflation exceeded that of the United States, resulting in significant real purchasing power loss for euro holders. The Australian dollar's real returns were mixed—nominal depreciation combined with elevated inflation created negative real returns for most of the period. The New Zealand dollar experienced similar dynamics. Gulf currencies, through currency stability and low inflation, delivered exceptional real returns to savers and investors, as they maintained their value while preserving purchasing power. The yen presented a paradox: despite depreciating significantly against the dollar, its near-zero inflation meant yen-denominated savings maintained purchasing power better than nominal exchange rates suggest. The Brazilian real, despite volatility, benefited from elevated interest rates that compensated for inflation, making it attractive for yield-seeking investors despite currency fluctuations.

Impact on Citizens and Quality of Life

Currency depreciation combined with high inflation creates severe consequences for ordinary citizens. In the eurozone, particularly in southern European nations, citizens experienced eroding real wages and reduced purchasing power despite relatively stable euro valuations. British households faced significant real income declines, as wage growth lagged inflation, particularly affecting lower and middle-income workers. In the United Kingdom, real household disposable income declined during 2022-2023, exacerbated by energy price spikes. Australian and New Zealand residents experienced similar pressures, with housing affordability deteriorating as currency weakness increased import costs while wages failed to keep pace with inflation. In contrast, Swiss citizens benefited from currency strength and low inflation, maintaining or improving purchasing power. Citizens in Gulf nations enjoyed stability and rising real incomes due to low inflation and currency predictability. Japanese citizens experienced wage stagnation but benefited from price stability and a strong yen abroad, making international travel and imports relatively affordable. Brazilian citizens faced significant real income erosion, as inflation exceeded wage growth despite attempts by the central bank to stabilize the currency through interest rate increases.

Investment Returns and Currency Appreciation Strategies

For investors evaluating currency exposure, the past decade offered vastly different opportunities across regions. Swiss franc appreciation, combined with negative real interest rates in Switzerland, meant currency gains often offset interest rate losses for Swiss franc investors. The pound sterling provided mixed returns—while depreciation eroded value, elevated interest rates partially compensated early in the period. Euro-denominated investments suffered from both currency depreciation and modest interest rates relative to inflation. Australian and New Zealand dollars offered elevated interest rates that partially compensated for currency weakness, attracting carry trade investors. However, these high interest rates reflected inflation risk premiums rather than genuine wealth creation. Gulf currencies provided stability without appreciation, unsuitable for capital appreciation but excellent for capital preservation. The yen offered an unusual opportunity: despite depreciation, the carry trade—borrowing yen at near-zero rates and investing in higher-yielding currencies—generated substantial returns until the Bank of Japan's policy shift in 2023-2024. The Brazilian real, despite volatility, provided exceptional returns to investors willing to accept currency risk, as interest rates exceeded 10 percent for much of the period, compensating for inflation and currency fluctuations.

Best and Worst Currency Investments

The Swiss franc emerges as the decade's best-performing currency for wealth preservation and real returns. Investors who held Swiss francs benefited from appreciation, low inflation, and economic stability. The New Zealand dollar, despite nominal depreciation, provided strong real returns through elevated interest rates that exceeded inflation by meaningful margins for much of the period. The Brazilian real offered exceptional nominal returns for those timing entry correctly, with interest rates providing 6-8 percent real yield above inflation in various periods. Conversely, the euro underperformed significantly, combining depreciation with elevated inflation, creating negative real returns for most holders. The British pound, while more resilient than the euro, still delivered disappointing real returns due to inflation exceeding wage and investment returns. The Australian dollar struggled similarly, with depreciation and elevated inflation creating real purchasing power losses. The Japanese yen, despite depreciation, paradoxically protected wealth through price stability, though nominal returns disappointed. The Canadian dollar and Swedish krona, outside our primary focus, similarly underperformed due to inflation pressures despite stable exchange rates.

Economic Conditions Determining Currency Strength

Certain factors consistently predicted currency strength across the decade. Central bank credibility and independence—exemplified by the Swiss National Bank and Federal Reserve—enabled currencies to appreciate and maintain value. Commodity export capacity, particularly in Gulf nations, provided currency support through consistent export revenues and trade surpluses. Fiscal discipline and low government debt ratios strengthened currencies by reducing inflation risks and central bank pressure for monetization. Interest rate differentials attracted capital flows, though elevated rates often reflected inflation risk premiums rather than genuine investment returns. Demographic trends mattered substantially: aging populations in Japan and parts of Europe created structural headwinds, while younger populations in emerging markets offered growth potential despite near-term inflation challenges. Geopolitical stability enhanced currency valuations, as safe-haven flows strengthened Swiss francs and diminished emerging market currencies during crises. Energy independence and commodity export capacity proved critical, with energy importers facing persistent depreciation pressures.

The Worst-Performing Currencies Globally

While our analysis focused on the world's strongest currencies, context demands acknowledging the worst performers. The Turkish lira experienced catastrophic depreciation, losing approximately 90 percent of its value against the US dollar between 2016 and 2026, as inflation reached 61 percent in 2023 and macroeconomic mismanagement accelerated currency collapse. The Argentine peso similarly collapsed, depreciating more than 95 percent against the dollar, with inflation exceeding 200 percent in 2023 alone, destroying savings and creating severe economic hardship. The Venezuelan bolívar, through hyperinflationary collapse, lost essentially all value, becoming economically irrelevant as the economy dollarized. The Lebanese pound, pegged theoretically to the dollar but abandoned in practice, lost 95 percent of its black-market value as capital controls and banking system collapse destroyed the currency's credibility. These currencies demonstrate the catastrophic consequences of fiscal mismanagement, central bank politicization, capital flight, and loss of institutional credibility—serving as cautionary tales for investors and policymakers.

Conclusion: Lessons for Investors and Policymakers

The past decade's currency dynamics reveal that sustainable currency strength requires multiple supporting factors: central bank credibility, fiscal discipline, low inflation, structural economic competitiveness, and institutional stability. The Swiss franc's outperformance reflects not luck but consistent policy discipline and economic management. The euro's underperformance stems not from fundamental design flaws but from disparate inflation experiences across member states and delayed policy response. The pound's struggles reflect both Brexit-related structural challenges and global inflation pressures. For investors, currency selection demands evaluating real returns rather than nominal appreciation, considering inflation differentials alongside exchange rate movements. The period from 2016-2026 demonstrates that nominal currency strength often masks real purchasing power erosion when inflation is elevated. Going forward, investors should prioritize currencies backed by central banks with demonstrated credibility, nations with fiscal discipline and low debt ratios, and economies with structural competitiveness. The stark contrast between the world's strongest currencies—maintaining stability and purchasing power—and the worst performers—experiencing hyperinflationary collapse—underscores that currency outcomes are not random but reflect deliberate policy choices and institutional quality.

References

International Monetary Fund (IMF). (2026). World Economic Outlook Database.

Federal Reserve Economic Data (FRED). (2026). Historical Exchange Rates and Inflation Data.

Bank for International Settlements (BIS). (2024). Quarterly Review on Currency Markets and Monetary Policy.

Organisation for Economic Co-operation and Development (OECD). (2026). Main Economic Indicators Database.

European Central Bank (ECB). (2026). Statistical Data Warehouse.

Bank of England. (2026). Monetary Policy Reports and Historical Data.

Swiss National Bank (SNB). (2026). Annual Economic Reports and Data.

Reserve Bank of Australia (RBA). (2026). Statement on Monetary Policy.

Reserve Bank of New Zealand (RBNZ). (2026). Monetary Policy Statements.

Central Bank of Brazil (Banco Central do Brasil). (2026). Relatórios de Inflação e Câmbio.

The Economist Intelligence Unit. (2026). Country Reports and Currency Analysis.

Trading Economics. (2026). Global Macro and Currency Data Platform.

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy