The U.S. Macroeconomic Inflection: Inflationary Persistence and Geopolitical Volatility Through 2026

USA

ECONOMY

By Marcelo Salamon

5/12/20263 min read

Abstract

This analysis examines the structural shifts in the United States economy as of mid-2026, focusing on the convergence of exogenous energy shocks and endogenous labor market resilience. Despite the S&P 500’s recent performance, the deviation between equity valuations and macroeconomic fundamentals suggests a period of significant repricing. This paper explores the "higher-for-longer" interest rate paradigm, the inflationary transmission mechanisms of the Middle Eastern conflict, and the liquidity sensitivity of digital assets like Bitcoin. The findings suggest that market equilibrium will remain elusive, favoring a regime of high volatility over a sustained bullish trend.

Introduction: The Divergence of Fundamentals and Euphoria

Global capital markets are navigating a profound paradox. While the S&P 500 reached record levels driven by the expansion of Multiples in the Technology sector, the underlying macroeconomic foundation has begun to show signs of structural fatigue. The transition from a "soft landing" narrative to one of inflationary re-acceleration has forced a reassessment of risk premiums. As of May 2026, the primary challenge remains the recalibration of market expectations against a Federal Reserve that is constrained by non-transitory price pressures.

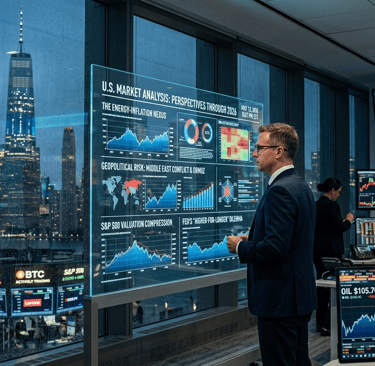

The Energy-Inflation Nexus and Geopolitical Risk

The resurgence of the Consumer Price Index (CPI) is not merely a byproduct of domestic demand but a direct consequence of systemic supply shocks. The sustained elevation of crude oil prices—exceeding $100 per barrel—functions as a regressive tax on global consumption.

Supply Chain Disruptions: The volatility in the Strait of Hormuz has reintroduced a "geopolitical risk premium" into energy markets.

Secondary Effects: Beyond direct fuel costs, high energy prices are infiltrating the Producer Price Index (PPI) through logistics, industrial manufacturing, and nitrogen-based fertilizer production, ensuring that inflation remains "sticky" across the broader economy.

Monetary Policy and the Resilience of the Labor Market

The Federal Reserve faces a "Dual Mandate" dilemma. Although inflation remains above the 2% target, the U.S. labor market has demonstrated unexpected durability.

The Unemployment Lag: Low unemployment rates provide the Fed with the "political and economic cover" to maintain restrictive interest rates.

The Yield Curve: The persistent inversion or flattening of the yield curve reflects a market that is skeptical of long-term growth while bracing for short-term liquidity tightening. Consequently, the "Fed Pivot" (the shift to cutting rates) has been deferred, as premature easing could risk a secondary inflationary wave reminiscent of the 1970s.

Asset Class Vulnerability: S&P 500 and the Liquidity Filter

The bull market of early 2026 was largely fueled by the "AI Revolution" and robust corporate earnings. However, high interest rates exert a gravity-like effect on Discounted Cash Flow (DCF) models.

Valuation Compression: As the Risk-Free Rate (Treasury yields) remains elevated, the Equity Risk Premium becomes less attractive, prompting institutional rotation from growth stocks to defensive postures and fixed income.

Bitcoin as a Liquidity Proxy: Bitcoin continues to behave as a high-beta asset. While its narrative as "Digital Gold" persists, its price action remains highly correlated with M2 Money Supply and global liquidity cycles. In a restrictive monetary environment, the cost of carry increases, often leading to de-leveraging events in the crypto-asset space.

Probabilistic Scenarios Through Year-End 2026

To provide a robust outlook, we must weigh three distinct economic trajectories:

Stagnation and Lateralization (Base Case): A period of "muddle through" where inflation remains between 3%–4%, preventing rate cuts but avoiding a full-scale recession. Markets remain range-bound with high intraday volatility.

The Supply-Side Shock (Pessimistic Case): An escalation in regional warfare leads to oil surpassing $120, forcing the Fed to resume hiking rates. This would likely trigger a systemic Bear Market and a significant contraction in consumer discretionary spending.

The Productivity Miracle (Optimistic Case): Gains from AI implementation begin to show in national productivity statistics, offsetting wage-push inflation and allowing for a controlled descent in rates without economic cooling.

Conclusion

The U.S. economy has transitioned from a recovery phase into a zone of heightened macroeconomic fragility. The interplay between persistent inflation, geopolitical friction, and the Federal Reserve’s restrictive stance has created a "low-visibility" environment for investors. For the remainder of 2026, the primary determinant of market direction will be the stabilization of energy costs. Until a clear disinflationary trend emerges, the risk-reward profile for equities and digital assets remains skewed toward the downside, necessitating a strategy centered on capital preservation and risk management.

Para complementar o seu relatório de análise econômica de meados de 2026, aqui estão as referências bibliográficas estruturadas seguindo um padrão acadêmico/institucional, refletindo o cenário de tensões geopolíticas, política monetária e volatilidade de mercado abordado no seu texto.

Bibliography (2026 Economic Briefing)

Federal Reserve Bank of St. Louis. The Economic Outlook and Monetary Policy: Risks to the Dual Mandate. (May 2026).

J.P. Morgan Global Research. 2026 Labor Markets at a Crossroads: AI Adoption and Geopolitical Friction. (April 2026).

Peterson Institute for International Economics (PIIE). Global Economic Implications of the 2026 Middle East Conflict: Energy Shocks and Growth Projections. (May 2026).

University of Michigan. United States Economic Outlook: 2026-2028 Forecast. (May 2026).

U.S. Department of the Treasury. Economic Policy Statements to the Treasury Borrowing Advisory Committee (TBAC). (Q2 2026).

World Bank Group. Global Economic Prospects: Growth Revisions Amid Geopolitical Instability. (June 2026).

Bitcoin Suisse Research. Crypto Outlook 2026: Institutional Integration and Macro Liquidity Dynamics. (2026).

Contact

Newsletter

contact@economicfinanceworldwide.com

Fone: +55 54 991220659

© 2026. All rights reserved. https://economicfinanceworldwide.com/privacy-policy